The Leverage Revolution in Manufacturing

Walk into any smartphone store today and you’ll be met with a paradox. For roughly the same €1,000 price tag as a decade ago, you now hold in your hand a device that can edit videos in 4K, generate images from text, navigate you across the globe, and connect you instantly with billions of people. The deflationary power of technology is astonishing. Every new wave of hardware and software delivers more for less.

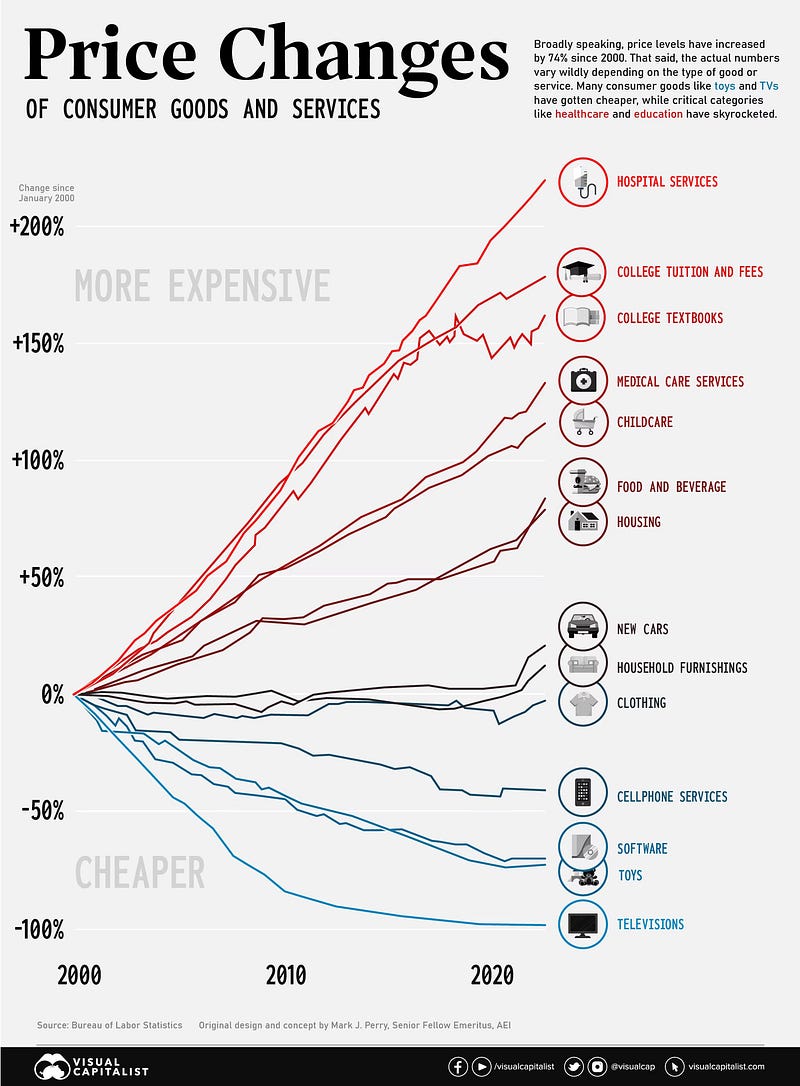

Manufacturing shares that same DNA. Over the past half-century, the cost of goods has dropped relentlessly, lifting global living standards. We don’t often frame it this way, but manufacturing is the original deflation engine of the modern world.

And yet, if you look beyond the falling prices, you discover a tension that defines our time: wages in technology have surged, while wages in manufacturing have stagnated. The people building the software platforms and digital services enjoy rising incomes; the people building the physical goods behind those screens have not.

This isn’t just a curiosity of economics. It is a structural imbalance — one that tells us about how value is distributed, how societies evolve, and what the next revolution in work might look like.

The paradox of deflation and wages

Both manufacturing and tech are deflationary. But the pathways they took diverged sharply.

In manufacturing, the past twenty years were dominated by offshoring. Companies searched for the lowest-cost labor, moving production from Europe or the US to China, then to Vietnam, and now to even lower-wage geographies. The cost of a T-shirt dropped, not because the process of making a T-shirt became radically more efficient, but because wages in Bangladesh are lower than in Lyon.

Meanwhile, in tech, productivity came from innovation and scale. The cost of delivering an extra software copy is near zero. Platforms multiplied distribution: one line of code written in San Francisco runs instantly on billions of devices worldwide. That scale translated into leverage — and leverage translated into wages.

A talented engineer in a factory could improve the efficiency of one production line. A talented engineer at Google could improve the experience of billions. The paychecks diverged accordingly.

How leverage works

Leverage is one of those words that hides an enormous amount of power. In finance, it means doing more with less capital. In technology, it means doing more with the same brain.

Consider a factory programmer who writes code to optimize a machine’s cycle time. The impact is real, but bounded: one machine, in one facility, maybe saving thousands of euros per year. Now consider an engineer tweaking the news feed algorithm at a social media giant. That single adjustment shapes the daily experience of billions of users. The value creation is exponential — and so is the compensation.

For years, manufacturing lacked this kind of leverage. The work was localized, the impact constrained by the walls of the factory. Even when digitization crept in, the scale of improvement stayed limited: a new MES here, a scheduling software there.

But something is shifting.

The quiet revolution on the shopfloor

In dozens of factories we’ve visited, we’ve seen a new pattern emerge. Manufacturing jobs that used to be highly localized are becoming more leveraged.

A coder no longer writes instructions for one robot in one building. Today, the same code can orchestrate dozens of robots across plants in multiple countries. A scheduling algorithm can balance global production, not just a single workshop. A predictive maintenance model can protect entire fleets of machines.

What used to be the domain of “one plant, one person” is turning into “one team, global footprint.”

This shift mirrors what happened in software twenty years ago. Developers stopped writing isolated programs and began writing platforms. Once leverage entered the picture, value creation exploded — and so did salaries.

The precursors for this happening are :

- Cost of line of code is going down thanks to AI. Hence, what previously was not economical to be automated is becoming automated ;

- Context uncertainty and level of data cleanliness to be able to operate has drastically changed with LLMs. Hence, what used to be uneconomical to structure as context and thus was operated by humans is getting operated by software, controlled by humans.

We’re starting to glimpse the trajectory of tech in industry.

Case in point: the compressed supply chain

Take one of the new fast-fashion giants. Whatever one thinks of their aesthetics or sustainability record, their operational model is astonishing. The company runs a global supply chain with a fraction of the white-collar staff employed by its competitors. Where a traditional brand might employ hundreds in procurement, planning, and merchandising, they do it with tens.

The reason is leverage. AI proposes designs. Algorithms make sourcing decisions. Data science predicts demand and allocates production. Human labor in the supply chain office is replaced by software and AI. Each person is multiplied.

This is the future: fewer jobs, but each amplified by technology to a scale previously unthinkable.

What this means for economic structure

There is a fundamental shift in white collar and production equation when the relationship between number of white collars and economical output is not linear.

It means concentration in fewer actors (because of greater economies of scale), race to the top (ie war for talents is increased when one individual can better your supply chain system by 1% with relatively low friction).

All dynamics that tech companies are well familiar with, but that manufacturing executives are discovering.

What this means for wages

If the offshoring era was defined by moving work to where wages were lowest, the leverage era will be defined by paying the best people for the job and increasing leverage.

Factories will still need hands on the shopfloor — automation is advancing, but it is not replacing the diversity of human skills any time soon. What will change dramatically is the profile of white-collar roles in industry.

This is another secret of reshoring and the new economical equation : for almost every vertical (ie everything not textile), the cost disadvantage of high-cost of labour countries is concentrated in white collars, not blue ones.

Instead of hundreds of clerks managing procurement manually, there will be a handful of data-savvy professionals orchestrating flows through software. Instead of dozens of engineers troubleshooting machines one by one, there will be small teams deploying algorithms across entire production networks.

The result: fewer roles overall, but higher wages for those who master the skills of code, data, and systems thinking. Manufacturing will no longer lag behind technology in income; it will converge — but on the condition that workers upskill into these new, more leveraged functions.

A shift in skills, not just headcount

The real discontinuity is not just quantitative — fewer people — but qualitative. The jobs that remain will be different in nature.

They will look less like clerical paperwork and more like software engineering. They will require comfort with abstraction, data manipulation, and systems architecture. They will reward the ability to automate repetitive intellectual work, not perform it.

This is not to say that all factory staff need to become coders. But it does mean that the archetype of the “white-collar industrial worker” is changing. Where once it was about diligence in repetitive tasks, tomorrow it will be about creativity in leveraging machines, algorithms, and networks.

Anecdotically, we are seeing in multiple companies we are building alongside manufacturing executives right now that the bottleneck is finding, upskilling, providing the right tools to, those white collars.

We’ve already seen this on the shopfloor. The “local nerd” who codes VBA scripts to keep the plant running, or hacks Arduino boards to connect machines, is becoming the most valuable person in the building. Technology is giving her the ability to scale her ingenuity across multiple sites. One factory director once told me that without their Excel wizard, production would literally grind to a halt. The wizard blushed. The rest of the team just nodded knowingly — half in admiration, half in fear of what would happen if she ever decided to take a long vacation.

The macroeconomic picture

Zooming out, this revolution has profound implications for the structure of economies.

For decades, advanced economies worried about manufacturing jobs disappearing offshore. That was the political story of the 1990s and 2000s: shuttered factories, hollowed-out towns, dislocated communities. Wages were flat because the competitive lever was always “find cheaper labor elsewhere.”

But if leverage replaces offshoring as the core driver of cost reduction, then the geography of production could shift again. Suddenly, it might matter less whether a factory is in Shenzhen or Stuttgart, because the differentiator isn’t labor cost but algorithmic leverage. A single engineer in Europe could control operations in Asia.

In this world, manufacturing wages might not be a race to the bottom. They could become a race to the top — for those with the right skills.

Lessons from history

This wouldn’t be the first time leverage reshaped industry. The original Industrial Revolution was precisely that: machines amplifying human labor. One weaver with a mechanical loom could do the work of ten. The cost of textiles collapsed, wages for skilled operators rose, and society reorganized around new roles.

The digital revolution did the same for information. One coder with global distribution channels could impact billions.

What we are witnessing now is the convergence of those two forces: the industrial leverage of machines meeting the digital leverage of code. The shopfloor is no longer an island of localized work; it is a node in a global network.

The risks ahead

Of course, revolutions are not smooth. For every factory that manages to upskill its workforce and embrace leverage, others will struggle. Some communities may see white-collar manufacturing roles disappear without replacement. The social contract around industrial work will need to be rewritten.

There is also a risk of polarization. Highly skilled data scientists and coders may thrive, while mid-level administrative staff see their roles automated away. Without intentional reskilling, we risk creating an even sharper divide between high-wage and low-wage work.

But if history is a guide, the path is not inevitable. Policy, education, and above all, the entrepreneurial ecosystem can shape outcomes. We can choose to build pathways for workers to move into higher-leverage roles, rather than leaving them behind. And if we don’t, we shouldn’t be surprised when the factory’s Excel wizard becomes mayor out of sheer necessity.

Why this matters for builders

For those of us building companies in the industrial space, this moment is electric. We are not simply making factories a bit more efficient. We are participating in a structural shift in how work is organized, how wages are distributed, and how productivity is created.

The challenge is enormous. We are redesigning systems that have been stable — or stagnant — for decades. But the opportunity is larger still.

Every startup that enables one worker to leverage machines across sites, every product that transforms clerical tasks into data science, every algorithm that scales globally, is not just creating value for a company. It is rewriting the social contract of industry.

A closing reflection

It is tempting to view deflation, wages, and leverage as technical matters for economists. But they are deeply human. Behind every curve and chart are workers, families, and communities.

The smartphone in your pocket, the shirt on your back, the car you drive — all are artifacts of a deflationary engine called manufacturing. The question is not whether this engine will keep running, but who benefits from the value it creates.

For the past generation, the answer was consumers (through lower prices) and tech workers (through higher wages). The next generation could be different. With leverage rising in factories, manufacturing workers themselves — at least those who embrace the new skills — could finally see wages rise in line with the value they create.

It is an extraordinary time to be involved. As builders, as investors, as operators, we have the privilege — and the responsibility — to help steer this shift.

Let’s build.