A lot has been written lately about rising geopolitical tensions. It’s often abstract, macro, and far away from the daily reality of companies. I want to tell a more concrete story — one informed by thousands of hours spent on factory floors across Europe and the US, working side by side with industrial leaders who are quietly rethinking where, how, and why they produce, and ambitious tech founders building the future of reshoring, one solution at a time.

This is what reshoring and geopolitical fragmentation look like when you zoom all the way in.

This also comes from a builder perspective : we build alongside our industrial and founder partners. Fourty plane flights a year on average for the writer of those lines. It means reality is messy and those lines are our best thinking as of Jan 2026. Things will change.

Lessons from history : production has always been the bottleneck

For as long as wars have been fought, production has been decisive. There’s a famous saying that wars are won through logistics — but logistics is downstream of something more fundamental: the ability to build. To design, industrialize, and manufacture at scale.

It’s why the question of industrial capacity is no longer confined to defense contractors. It’s now front of mind for consumer goods, electronics, chemicals, automotive, and textiles. Everyone has understood, sometimes painfully, that if you cannot produce — or cannot reconfigure production fast enough — you are exposed. COVID also taught most of us a thing or two about this.

Everything is dual-use now

One striking shift we observe is how blurred the line has become between civilian and strategic technologies. AI is the obvious example, but it goes far beyond that. The drone revolution was kickstarted not by a defense prime, but by a consumer electronics company: DJI.

This reality changes everything. Governments are no longer just regulating “defense” sectors; they are increasingly attentive to the footprint of consumer products, software stacks, data flows, and industrial dependencies. Industrial leaders feel this pressure directly — in export controls, procurement rules, and political scrutiny that simply didn’t exist a decade ago.

Scale matters — again

History again is instructive here. During the Second World War, victory was not just about better ideas, but about scale. Automotive giants retooled and produced at volumes that changed the course of history because they had three things: talent density, access to raw materials, and an installed CAPEX base.

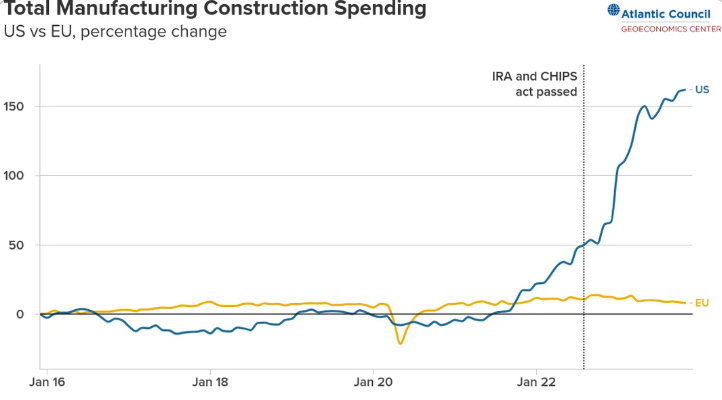

Fast forward to today, and you see echoes of this logic. The race to build new factories in the US is staggering (see chart).

We’re seeing massive concentration efforts in strategic supply chains — semiconductors, data centers, energy infrastructure. More quietly, we’re even seeing early signs of textile reshoring, something that would have sounded naïve not so long ago.

The difference this time is technology. Automation and AI are changing the cost equation fast. In some activities, output is becoming partially decorrelated from human labor. That changes where it makes sense to build — and at what scale.

From globalization to fragmentation — and “friendshoring”

No serious industrial leader believes in a single, global, frictionless supply chain anymore. Fragmentation is now the base assumption. What replaces it is not autarky, but choice: friendshoring.

We see companies explicitly choosing their dependencies, mapping political risk alongside cost, lead time, and quality. Blocks are forming quickly. Supply chains are being redesigned not just for efficiency, but for resilience and optionality.

We also see the rise of deals : at the highest level, everything is a deal about what to do and with whom to do it. We also see that partnering with a supplier is less about a contractual obligation and a shared destiny contract : for the next 10 to 15 years, both the client and the supplier pledge to go through this troubled time together.

This translates into the software stack : most supply chains are undergoing a deep integration through continuous flow of data. The bets are huge and mutual. There’s no light touch partnerships in an uncertain world.

The blind spot: product design in the age of uncertainty

One of the biggest blind spots we still encounter is product development. On the ground, the most advanced industrial players are rethinking their products themselves — not just their factories locations.

There’s a joke we keep telling : trying to rethink an industrial footprint without rethinking the product is like chocolate-covering broccoli. It might look nicer, but it doesn’t change the fundamentals. Most products come from a “world is flat, raw material is abundant, energy is cheap” era. That era is over — but the products stay.

We see forward-looking companies redesigning products to be more frugal, easier to industrialize, and compatible with simpler, more resilient supply chains. It’s deep re-engineering — and it’s where a lot of the real leverage lies. It’s also longer to execute — so the best are starting early.

Humility and parallel bets

Contrary to the caricature, the best industrial leaders are remarkably humble about the future. Very few claim to have “the answer.” Instead, they manage portfolios of bets: multiple geographies, multiple technologies, multiple supply chain configurations.

It’s realism. In a world where geopolitics, regulation, and technology evolve simultaneously, optionality becomes a strategic asset. We consistently see the companies with the highest agility win and be able to not only bet right, but also course correct in real time.

Technology as the great accelerator

What’s different this time — and what’s accelerating everything — is the pace of technological change. AI, automation, and advanced software stacks allow factories to be built faster, reconfigured more easily, and operated with fewer constraints tied to local labor markets.

This is why we see the rise of gigafactories in highly strategic locations. And it’s also why we see industrials behaving more like portfolio managers, continuously reallocating capacity, capital, and attention.

A fast-moving landscape

All of this is evolving incredibly fast. From where we stand, working with some of the best industrial players in the world, one thing is clear: the gap is widening.

The best are getting faster. They learn quicker, reconfigure more often, and are increasingly comfortable operating in uncertainty. Others struggle — not for lack of effort, but because the old mental models no longer hold.

We’re humbled to witness this transition from the inside. Reshoring is not a slogan. It’s a messy, strategic, deeply technical process — and it’s becoming one of the defining industrial challenges of our time.

Ultimately, we’re builders. That forces humility — and recognition that world may never be the same. The courage to see the world as it is, and the speed and excellence to do our part in steering it in the right direction.

Let’s build.